9 Easy Facts About Bankruptcy Attorney Tulsa Shown

9 Easy Facts About Bankruptcy Attorney Tulsa Shown

Blog Article

9 Easy Facts About Bankruptcy Lawyer Tulsa Explained

Table of ContentsA Biased View of Chapter 7 - Bankruptcy BasicsThe Ultimate Guide To Tulsa Debt Relief AttorneyThe Best Strategy To Use For Bankruptcy Lawyer TulsaSome Known Details About Bankruptcy Attorney Tulsa 8 Easy Facts About Chapter 13 Bankruptcy Lawyer Tulsa Explained

The statistics for the other primary type, Chapter 13, are even worse for pro se filers. Suffice it to say, speak with a legal representative or two near you who's experienced with insolvency regulation.Many lawyers also offer cost-free consultations or email Q&A s. Take advantage of that. Ask them if insolvency is certainly the right choice for your scenario and whether they believe you'll qualify.

Advertisement Now that you have actually decided bankruptcy is indeed the ideal course of action and you ideally removed it with a lawyer you'll need to obtain started on the documentation. Before you dive into all the main bankruptcy kinds, you ought to obtain your own records in order.

Tulsa Bankruptcy Legal Services for Dummies

Later down the line, you'll in fact need to verify that by disclosing all type of info about your economic events. Below's a fundamental checklist of what you'll require when driving ahead: Identifying records like your chauffeur's license and Social Safety and security card Tax returns (approximately the previous 4 years) Proof of revenue (pay stubs, W-2s, self-employed incomes, revenue from possessions along with any kind of earnings from federal government advantages) Financial institution statements and/or retirement account statements Proof of value of your possessions, such as car and property assessment.

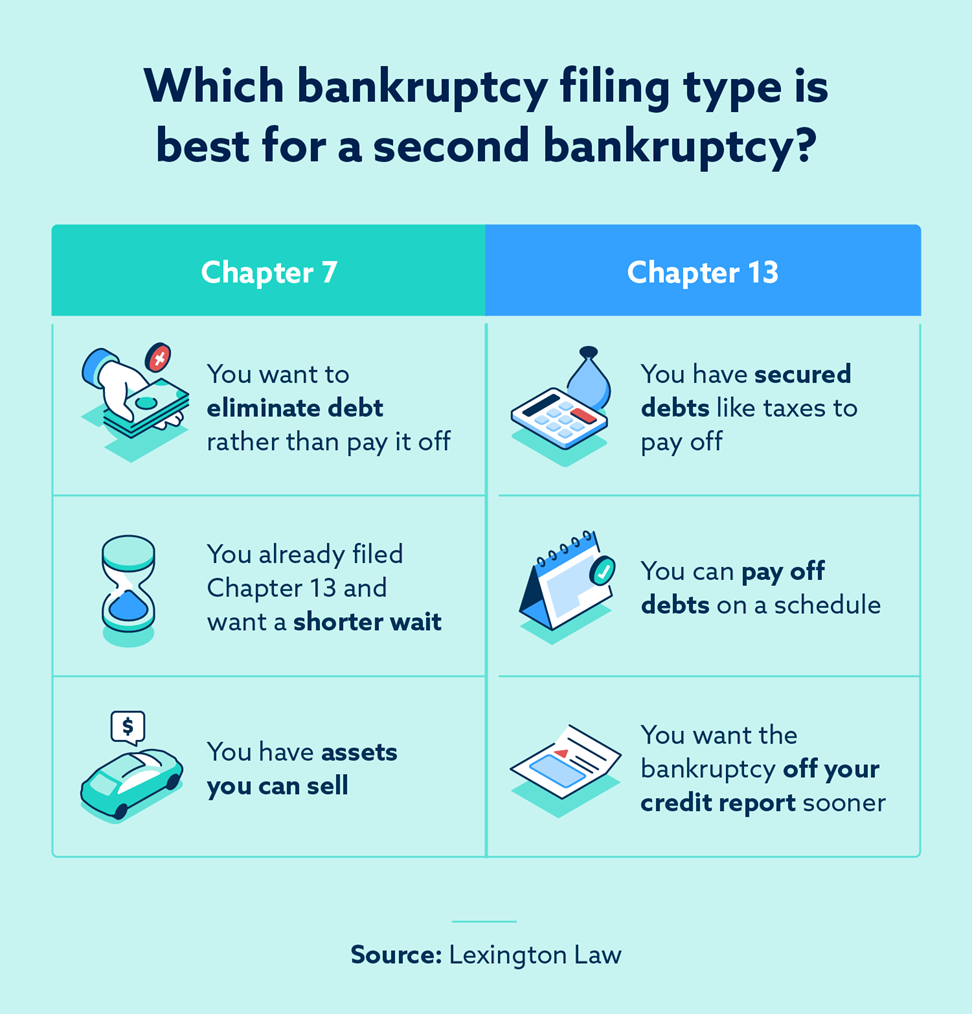

You'll want to comprehend what type of debt you're attempting to fix.

You'll want to comprehend what type of debt you're attempting to fix.If your revenue is expensive, you have another choice: Chapter 13. This option takes longer to settle your debts because it calls for a long-lasting payment strategy typically 3 to 5 years prior to a few of your continuing to be financial debts are wiped away. The declaring procedure is additionally a lot more intricate than Chapter 7.

How Tulsa Debt Relief Attorney can Save You Time, Stress, and Money.

A Chapter 7 bankruptcy stays on your credit score report for 10 years, whereas a Chapter 13 bankruptcy falls off after seven. Before you send your bankruptcy types, you should first complete an obligatory course from a credit counseling agency that has actually been authorized by the Division of Justice (with the noteworthy exception of filers in Alabama or North Carolina).

The program can be completed online, in individual or over the phone. Courses typically set you back between $15 and $50. You need to finish the course within 180 days of declare personal bankruptcy (Tulsa bankruptcy lawyer). Use the Department of Justice's site to find a program. If you stay in Alabama read the full info here or North Carolina, you should select and finish a training course from a listing of independently accepted providers in your state.

See This Report about Bankruptcy Attorney Tulsa

A lawyer will typically manage this for you. If you're filing by yourself, understand that there are about 90 different bankruptcy districts. Inspect that you're filing with the proper one based upon where you live. If your long-term home has relocated within 180 days of loading, you must submit in the area where you lived the higher portion of that 180-day duration.

Commonly, your bankruptcy attorney will work with the trustee, but you might need to send the person papers such as pay stubs, tax returns, and financial institution account and credit score card statements directly. An usual false impression with personal bankruptcy is that once you submit, you can stop paying your debts. While personal bankruptcy can help you wipe out many of your unsecured you can check here financial obligations, such as past due medical bills or personal loans, you'll want to maintain paying your month-to-month repayments for safe financial obligations if you desire to maintain the residential property.

How Tulsa Bankruptcy Filing Assistance can Save You Time, Stress, and Money.

If you're at risk of foreclosure and have actually tired all other financial-relief options, after that declaring Phase 13 may postpone the foreclosure and assist in saving your home. Eventually, you will still need the income to continue making future mortgage payments, in addition to settling any kind of late payments over the training course of your layaway plan.

If so, you might be called for to supply extra information. The audit can postpone any kind of financial obligation alleviation by numerous weeks. Naturally, if the audit shows up wrong information, your instance can be rejected. All that stated, these are relatively uncommon circumstances. That you made it this much while doing so is a decent indicator a minimum of some of your debts are qualified for discharge.

Report this page